Term sheets are a common part of the financing process for tech companies, whether they are raising equity or taking on debt. Many tech startups are familiar with the vocabulary used on an equity term sheet (from a VC or Angel) but debt term sheets will have some terms that may not be familiar.

In this post, I’ll go over some of the basic terms in a debt term sheet that you likely won’t see on an equity term sheet. Before deciding on financing with debt, I would also recommend considering all of the Pros and Cons of Debt, Equity and Bootstrapping to ensure that debt financing is the right fit for the company.

Why Term Sheets?

In Venture Deals by Brad Feld and Jason Mendelson, they point out that Term sheets are not actually a legal requirement. They are more or less a tool for negotiations, to focus discussions and to outline an offer. From Venture Deals: “Nothing requires a term sheet to be used. Our favourite negotiations with entrepreneurs have been ones where we’ve literally shaken hands and agreed on valuation, board structure, and option pool size verbally or over email“. Even with this in mind, term sheets provide value by aligning borrowers and lenders/investors early in the process. They point out later that “Usually, the term sheet will be the first real negotiated document in a relationship”.1

Cómo Funcionan las Tiradas Gratis en los Casinos según Gransuerte

Las tiradas gratis, conocidas en el sector como free spins, representan uno de los mecanismos promocionales más extendidos en la industria del juego en línea. Su funcionamiento, sin embargo, va mucho más allá de una simple ronda gratuita en una máquina tragamonedas. Detrás de cada tirada gratuita existe una estructura técnica, matemática y regulatoria que determina su valor real para el jugador. Comprender cómo operan estos incentivos permite tomar decisiones más informadas y evitar malentendidos sobre lo que realmente ofrecen los operadores cuando incluyen estas promociones en sus catálogos de bonificaciones.

Qué son exactamente las tiradas gratis y cómo se estructuran técnicamente

Una tirada gratis es, en términos técnicos, una ronda de juego en una tragamonedas en la que el jugador no utiliza fondos propios de su saldo disponible. El casino asume el coste de esa ronda, aunque con condiciones específicas que varían según el operador y la normativa vigente en cada jurisdicción. No se trata simplemente de “jugar gratis”: existe un valor de apuesta predeterminado por giro, que el casino fija unilateralmente y que suele oscilar entre 0,10 € y 0,20 € por tirada en la mayoría de los operadores europeos.

Este valor de apuesta predeterminado tiene una implicación directa sobre las ganancias potenciales. Si un jugador recibe 50 tiradas gratis con un valor de 0,10 € por giro, el valor nominal total del bono es de 5 €. Sin embargo, las ganancias generadas por esas tiradas no suelen entregarse directamente como saldo disponible para retirar. En casi todos los casos, pasan a convertirse en saldo de bono, sujeto a requisitos de apuesta adicionales.

Los requisitos de apuesta, denominados en inglés wagering requirements, son el multiplicador que indica cuántas veces debe apostarse el saldo de bono antes de poder retirarlo como dinero real. Por ejemplo, si las ganancias de las tiradas gratis ascienden a 20 € y el requisito de apuesta es de 30x, el jugador deberá apostar un total de 600 € en juegos elegibles antes de que ese saldo se convierta en fondos retirables. Este multiplicador puede variar enormemente: en algunos operadores regulados dentro de la Unión Europea se sitúa entre 20x y 40x, mientras que en plataformas con licencias menos estrictas puede superar el 60x o incluso el 100x.

Otro elemento técnico relevante es la contribución de los juegos al cumplimiento del requisito de apuesta. Las tragamonedas suelen contribuir al 100%, pero las mesas de blackjack, ruleta o baccarat frecuentemente contribuyen solo entre un 5% y un 25%, lo que en la práctica hace que cumplir los requisitos con estos juegos sea considerablemente más lento y difícil.

Tipos de tiradas gratis según su origen y condiciones de activación

Existen distintas categorías de tiradas gratis según cómo se activan y cuál es su naturaleza jurídica dentro del contrato entre el casino y el jugador. La primera distinción fundamental es entre las tiradas gratis como parte de un bono de bienvenida y las tiradas gratis sin depósito. Las primeras requieren que el jugador realice un depósito inicial para activarlas, mientras que las segundas se otorgan sin necesidad de depositar fondos, aunque con condiciones de retiro habitualmente más restrictivas.

Las tiradas gratis sin depósito son especialmente populares como herramienta de captación de nuevos usuarios. Desde una perspectiva de marketing, permiten al operador ofrecer una experiencia del producto sin que el usuario asuma riesgo financiero inicial. No obstante, las condiciones asociadas suelen incluir límites máximos de ganancia retirable (frecuentemente entre 50 € y 100 €), requisitos de apuesta elevados y restricciones de tiempo para completar dichos requisitos, normalmente entre 3 y 7 días.

Las tiradas gratis activadas dentro del juego, conocidas como bonus spins o simplemente como rondas de bonificación, tienen una naturaleza diferente. Estas se activan mediante combinaciones específicas de símbolos dentro de una tragamonedas, como los símbolos de dispersión o scatter, y no están sujetas a requisitos de apuesta adicionales porque las ganancias se acreditan directamente como saldo real. Esta distinción es fundamental: las tiradas gratis dentro del juego tienen un valor intrínseco superior para el jugador en comparación con las tiradas promocionales ofrecidas por el operador.

Existe también una categoría intermedia: las tiradas gratis recargables o de fidelización. Estas se ofrecen a jugadores ya registrados como parte de programas de lealtad o promociones semanales. Plataformas como Gransuerte, que opera bajo un marco regulatorio europeo, incorporan este tipo de incentivos dentro de sus programas de bonificación habituales, permitiendo a los jugadores activos acceder a rondas adicionales en títulos seleccionados sin necesidad de realizar depósitos adicionales, aunque sujetas igualmente a condiciones específicas de uso.

Para quienes deseen profundizar en las condiciones concretas de cada tipo de promoción, la información detallada sobre cómo se aplican los requisitos en cada caso está disponible aquí, donde se detallan las condiciones vigentes para cada tipo de oferta según la normativa aplicable.

El marco regulatorio que rige las tiradas gratis en Europa

La regulación de las tiradas gratis ha evolucionado significativamente en la última década. En 2019, el Reino Unido fue uno de los primeros mercados en introducir restricciones específicas sobre las bonificaciones de casino, cuando la UK Gambling Commission comenzó a exigir mayor transparencia en los términos y condiciones de los bonos. Esta tendencia se extendió progresivamente a otros mercados europeos.

En España, la regulación del juego en línea está supervisada por la Dirección General de Ordenación del Juego (DGOJ), organismo que desde la aprobación de la Ley 13/2011 de Regulación del Juego ha ido actualizando sus normativas para adaptarse a las prácticas del sector. En 2020 y 2021, se introdujeron restricciones importantes sobre la publicidad del juego online, incluyendo limitaciones sobre cómo los operadores pueden comunicar sus bonificaciones, lo que afectó directamente a la forma en que se presentan las tiradas gratis al público.

La normativa española exige que los operadores con licencia DGOJ incluyan en toda comunicación promocional información clara sobre los requisitos de apuesta, el período de validez del bono y los juegos excluidos. Esta obligación de transparencia, aunque no elimina los requisitos de apuesta, sí obliga a los operadores a presentarlos de forma comprensible, evitando que se oculten en páginas de términos y condiciones de difícil acceso.

En Alemania, la situación es diferente. Desde la entrada en vigor del nuevo Tratado Interestatal sobre Juegos de Azar en julio de 2021 (Glücksspielstaatsvertrag 2021), los operadores con licencia alemana tienen prohibido ofrecer bonos de casino que incluyan tragamonedas, lo que en la práctica elimina las tiradas gratis como herramienta promocional en ese mercado. Esta decisión regulatoria fue especialmente relevante para el sector porque Alemania representaba uno de los mercados de mayor tamaño en Europa continental.

En contraste, mercados como Malta, a través de la Malta Gaming Authority (MGA), mantienen un enfoque regulatorio más permisivo, aunque con exigencias crecientes de transparencia. Muchos operadores europeos, incluyendo los que operan en múltiples jurisdicciones, cuentan con licencias MGA como base regulatoria, lo que les permite ofrecer productos en mercados donde la regulación local lo permite.

Gransuerte, como operador que trabaja dentro de un marco regulatorio definido, debe cumplir con los requisitos de transparencia exigidos por las autoridades competentes en cada mercado donde opera. Esto implica que las condiciones de sus tiradas gratis deben estar claramente documentadas y ser accesibles para el usuario antes de que este active cualquier promoción.

Cómo calcular el valor real de una tirada gratis y qué factores influyen en las ganancias esperadas

Calcular el valor real de una tirada gratis requiere entender el concepto de RTP (Return to Player o retorno al jugador) y cómo interactúa con los requisitos de apuesta. El RTP es el porcentaje del total apostado que una tragamonedas devuelve estadísticamente al jugador a lo largo del tiempo. Una tragamonedas con un RTP del 96% devolverá, en teoría, 96 € por cada 100 € apostados. Sin embargo, esta cifra es un promedio calculado sobre millones de rondas, por lo que en sesiones cortas la varianza puede ser enorme.

Para calcular el valor esperado de un conjunto de tiradas gratis, se puede utilizar la siguiente fórmula básica: valor de la tirada × número de tiradas × RTP = valor bruto esperado. Si las tiradas tienen un valor de 0,10 €, son 50 en total y el RTP del juego es del 96%, el valor bruto esperado sería 0,10 × 50 × 0,96 = 4,80 €. Sin embargo, a este cálculo hay que aplicar el impacto del requisito de apuesta.

Si las ganancias obtenidas (supongamos que el jugador tiene suerte y obtiene 15 €) están sujetas a un requisito de apuesta de 35x, deberá apostar 525 € antes de poder retirar. Con un RTP del 96%, cada euro apostado tiene un coste esperado del 4%. Por lo tanto, apostar 525 € tiene un coste esperado de 525 × 0,04 = 21 €. Dado que las ganancias iniciales eran de 15 €, el valor neto esperado de cumplir el requisito de apuesta sería negativo: el jugador perdería estadísticamente más de lo que ganó con las tiradas.

Este análisis matemático explica por qué los expertos en juego responsable insisten en que las tiradas gratis no deben considerarse una fuente de ingresos, sino una herramienta para explorar nuevos juegos con un riesgo financiero reducido. La volatilidad de las tragamonedas añade otro factor importante: los juegos de alta volatilidad ofrecen ganancias menos frecuentes pero de mayor magnitud, mientras que los de baja volatilidad ofrecen ganancias más frecuentes pero de menor cuantía. Para el propósito de cumplir requisitos de apuesta, los juegos de baja volatilidad son generalmente más adecuados porque permiten mantener el saldo durante más rondas.

La selección del juego en el que se aplican las tiradas gratis también influye significativamente en el resultado esperado. Los operadores suelen asignar las tiradas a títulos específicos, frecuentemente juegos nuevos o de alta popularidad, lo que no siempre coincide con los juegos de menor ventaja para la casa. Cuando el jugador tiene libertad de elegir el título, es recomendable optar por tragamonedas con RTP superior al 96% y volatilidad media o baja si el objetivo es maximizar las posibilidades de cumplir los requisitos de apuesta.

Otro factor que afecta al valor real de las tiradas gratis es el límite de ganancia máxima. Muchos operadores establecen un techo sobre las ganancias que pueden generarse a partir de tiradas gratis, independientemente del resultado real de las rondas. Este límite, que suele situarse entre 50 € y 200 €, protege al operador de pérdidas extraordinarias derivadas de grandes jackpots activados durante rondas gratuitas, pero también limita el potencial de ganancia del jugador incluso en los escenarios más favorables.

En definitiva, las tiradas gratis son un mecanismo complejo cuyo valor real depende de múltiples variables interrelacionadas: el valor por giro, el número de tiradas, el RTP del juego asignado, el requisito de apuesta aplicado a las ganancias, el período de validez, los límites de ganancia máxima y la volatilidad del título. Operadores como Gransuerte, que operan en mercados regulados, están obligados a proporcionar información clara sobre cada uno de estos parámetros, lo que permite al usuario hacer una evaluación informada antes de activar cualquier promoción. Comprender esta estructura no solo ayuda a gestionar mejor las expectativas, sino también a tomar decisiones de juego más conscientes y responsables dentro de los límites que cada uno se establezca.

Term sheets have, at times, been used to simply get a company’s attention and both investors and lenders develop a reputation on whether on not they close their term sheets. Siri Srinivas’s tweet mocks this practice beautifully. 2

Term Sheets are simply a tool for outlining in writing the terms and conditions being discussed. I have personally worked on deals with and without term sheets, but when using debt financing (rather than equity) it is extremely common to use a term sheet. This is because a term sheet can clearly outline to a borrower the general terms and conditions of an offer before being presented to a credit department or committee for approval.

With this in mind it’s important to understand where in the lending process the term sheet fits in.

Term Sheets vs Letters of Offer

Although term sheets are technically non-binding offers (sometimes even called “Discussion Papers” or “Letters of Intent“) they still form a great outline of what will be offered and are generally not presented unless the lender has a strong opinion that they would like to finance the company. Once a term sheet is presented, a lender will then underwrite the file and present it for review by a credit department (or committee), to be followed up by a binding Letter of Offer.

First Things First

Some of the vocabulary used in a debt term sheet is different from what many founders are familiar with on an equity term sheet. Here are some examples.

Amortization

- Amortization is a concept that will be different from an equity term sheet along with the interest rate. The loan will have to be payed back. The amortization is the length of the term that the loan can be payed back over. Amortizations may be as short as a few months (ei: Bridge Financing) or as long as 30 years (ei: for Real Estate Financing). Most amortizations for term loans will be 1-7 years.

Interest Rate

A major difference from an equity Term Sheet is that the financing will have an interest rate and requires repayment. The interest rate may be a Fixed Rate or a Floating Rate.

- Fixed-Rate: A fixed-rate will have a set interest and principal repayment amount each month. The downside is that it often comes with additional breakage fees, less flexibility, and if the banks prime rate drops the borrower does not benefit from this adjustment.

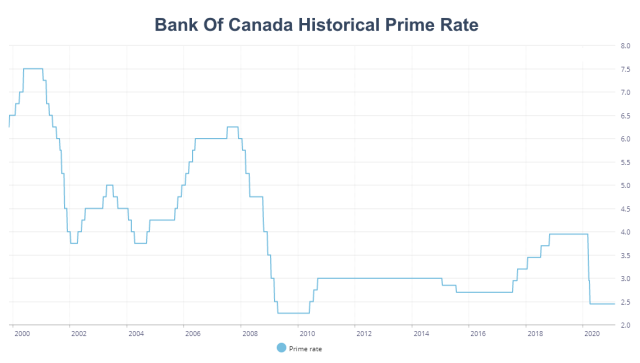

- Floating Rate: A floating rate will have a “Base Rate” that follows either the Bank of Canada’s Prime Rate, LIBOR (London Inter-Bank Offered Rate), or the lender’s own internal base rate. It will also have a “variance” which represents the lender’s spread (mark-up). It is important to understand which rate you are tracking too if you are on a floating rate. For floating rates, the principle is charged based on the amortization amount and the interest amount varies month to month.

Security

- When raising equity a portion of the company’s ownership is exchanged for the funds. Loans take no ownership but need to be secured.

- Types of security can include General Security Agreements (GSAs), registrations against specific Intellectual Property, Postponements of Claim, and Personal Guarantees. (I’ll go over the different types of security that can be offered or requested for debt term sheets in another post and what they each mean.)

Conditions Precedent

- These are conditions that will need to be met prior to the loan advancing. Examples may be a specific request additional due diligence – for example, an accountant prepared year-end financial statement or execution of a legal agreement (like an offer to purchase) that would have to precede the loan advancing.

- Another common condition precedent may be that a certain amount of equity is raised prior to the loan advancing. This condition might require the funds to either be deposited into the companies bank account first or proof that the funds are committed by the investor.

Covenants

- Covenants are one way a lender tracks a company’s performance. Some covenants can scare companies away if they are too restrictive. The goal of a well-determined covenant is that the borrower and the lender agree that it is both attainable enough to be met consistently and flexible enough to exist without impeding growth. It’s important to understand the covenants on any agreement and borrowers should feel free to ask a lender why they have chosen a specific covenant.

- There are three types of covenants, Positive, Negative, and Financial Covenants.

- Positive Covenants (or Affirmative covenant) is a promise to do or maintain. An example would be to maintain a certain level of working capital in the company.

- Negative Covenants are covenants to prevent a certain activity. An example of this might be a No Dividends or Withdrawals covenant for the term of the loan. This could be put in place to clarify that all of a loans funds are to stay in the company. There are many different types of covenants and they vary substantially.

- Financial Covenants reference maintaining a performance ratio like a Debt to Equity Ratio or a Debt Servicing Ratio (less common in tech) and is set to be met to help maintain the financial health of a company.

Reporting Requirements

- Loans are reviewed regularly with financial information provided by the company. This can be done annually, quarterly, or even on a monthly basis depending on the size of the loan and the complexity of the agreement.

- These reporting requirements would be listed on the Term Sheet or on the final Letter of Offer.

Prepayment Indemnity

A Prepayment Indemnity is a penalty for paying back the loan before the end of the amortization term.

It can show up in different ways but common types are:

- Months of Interest: in this method, a prepayment may carry a fee that is equal to a certain number of months interest on either the remaining balance or the drawn amount. These can vary from 3 months to 12 months or even higher.

- IRR Calculation: Lenders may have a set IRR (Internal Rate of Return) on their loans. If a loan is paid back early there may be a required return that is paid out calculated from the date of the loan’s advance to the date of the repayment. An example of this would be a 15% IRR requirement.

Participating in the Upside

There is a saying that goes “Equity owns the upside of a Deal and Debt owns the downside.”

What this means is that equity investing is highly focused on the success and growth of a company while lenders are highly focused on mitigating the downside risk – simply put, avoiding default situations. There are a few tools that can change this for a lender. These tools are Royalties, Warrants and Bonus/Kickers.

- Royalties: Royalties are a payment that is paid as a percentage of sales. They can be collected monthly, quarterly or annually. Sales growth is aligned between the lender and the company.

- Warrants: Warrants give the lender the option to buy shares at an agreed price on or before a specified date. The company and the lender are aligned in increasing valuation. 5

- Bonus (or Kicker): This is a one-time payment that is made at the end of the term. It is often used when the lender has taken a longer interest-only period. The company and lender are aligned for the full term of the loan for the bonus to be paid at maturity.

Using any of these tools, means that a lender is not just underwriting and trying to mitigate the risk of default, but is also lending to the company on the basis that they believe strongly in the companies success. These options can really align both the lender and the founder’s motivations to have the company succeed.

Summary

- There are different terms and meanings used on a debt financing term sheet vs. an equity financing term sheet.

- Ask your lender for clarifications and check if there are definitions in an appendix to the contract.4

- Understand terms that help lenders participate in the “upside” of a deal (Royalties, Warrants and Bonus/Kickers).

- Considering the Pros and Cons of Debt and Equity when looking at financing options.

Footnotes

(1) Venture Deals by Brad Feld and Jason Mendelson – Page 253. Its also one of the First 5 books I recommend for learning about Tech Finance.

(2) Siri Srinivas is an early stage investor at @drapervc

(3) Graph from Credit Genius Article

(4) I will elaborate on these specific options in a future post. In the meantime, here is a great article on Warrants by K. Reilly of Fuse Capital

(5) Also please keep in mind that this is a guide and the specific terms may be defined in an appendix to your offer

(6) Here is another great guide to some of the more complex terms that will show up on a Debt term sheet. A guide to important terms in a debt term sheet by Rohit Mittal