Canada Emergency Business Account (CEBA) Loans

If you’re a business that is holding an outstanding CEBA loan due by December 31, 2023 we have everything you need to know about CEBA loans. Levr.ai can also help you learn more about what options are available to ensure you get as much CEBA loan forgiveness (free money) as possible!

Table of contents

Small businesses are the heart and soul of our communities, providing employment opportunities, fostering innovation, and driving economic growth. During times of crisis, such as the COVID-19 pandemic, small businesses often face significant challenges.

Supporting small businesses is about nurturing the spirit of entrepreneurship and empowering individuals to pursue their dreams. It’s about fostering a culture of innovation, creativity, and self-reliance.

CEBA Canada Emergency Business Account (CEBA) was organized and rolled out in December 2020 to stay afloat, pay their employees, and cover their operational expenses. By investing taxpayer dollars in supporting these businesses, governments recognize the immense value they bring to our society and seek to protect them from economic devastation.

By assisting small businesses, governments help create a supportive environment where entrepreneurs can flourish, leading to job creation, economic stability, and a vibrant business ecosystem.

Hur gratissnurr fungerar enligt CasinosFreeSpins experter i Sverige

Gratissnurr, eller free spins som de ofta kallas inom casinobranschen, är ett av de vanligaste bonuserbjudandena på svenska spelmarknaden. Trots att begreppet är välkänt bland spelare finns det många aspekter av hur gratissnurr faktiskt fungerar som sällan förklaras på ett transparent och pedagogiskt sätt. Experterna på CasinosFreeSpins har under åren analyserat hundratals erbjudanden och identifierat de mekanismer som avgör om ett gratissnurr-erbjudande faktiskt är fördelaktigt för spelaren eller om det i praktiken är svårt att omsätta till riktiga vinster. Den här artikeln går igenom de tekniska och regulatoriska grunderna bakom gratissnurr, hur omsättningskrav fungerar i praktiken, vilka regler som styr marknaden i Sverige och vad spelare bör känna till innan de accepterar ett erbjudande.

Vad är gratissnurr och hur aktiveras de tekniskt?

Ett gratissnurr är i grunden en möjlighet att snurra ett spelautomathjul utan att använda egna pengar. Spelaren tilldelas ett visst antal snurr på en eller flera specificerade spelautomater, och eventuella vinster läggs till spelarens konto i form av bonuspengar eller, i vissa fall, direkt som riktiga pengar. Skillnaden mellan dessa två utfall är avgörande och något som ofta missas i den initiala presentationen av erbjudandet.

Tekniskt sett aktiveras gratissnurr antingen automatiskt vid registrering, efter en insättning som uppfyller ett minimikrav, eller via en kampanjkod som spelaren anger manuellt. Casinoplattformar använder sig av bonussystem som är integrerade i deras spelhanteringsprogram. När en spelare kvalificerar sig för ett erbjudande registreras detta i systemet och snurren kopplas till spelarens konto med specifika parametrar: antal snurr, insatsvärde per snurr, vilka spel som är tillåtna och hur länge erbjudandet är giltigt.

Insatsvärdet per gratissnurr är en av de viktigaste parametrarna. Det är vanligt att gratissnurr har ett fast värde per snurr, exempelvis 1 krona eller 5 kronor. Detta innebär att oavsett vilket spel spelaren väljer att använda snurren på, beräknas vinsterna utifrån detta fasta belopp snarare än spelarens normala insatsnivå. Om en spelare vanligtvis spelar med 20 kronor per snurr men gratissnurren har ett värde av 1 krona, är den potentiella vinsten per snurr avsevärt lägre än vad spelaren är van vid.

Spelautomaternas RTP, Return to Player, påverkar också utfallet av gratissnurr. RTP är ett statistiskt mått som anger hur stor andel av de insatta pengarna som i genomsnitt betalas tillbaka till spelarna över tid. En spelautomat med 96 procents RTP betalar i teorin tillbaka 96 kronor för varje 100 kronor som satsas. Gratissnurr på spel med hög RTP är därmed statistiskt mer fördelaktiga än på spel med lägre RTP. Experter på CasinosFreeSpins rekommenderar alltid att kontrollera RTP-värdet på de spel där gratissnurren gäller, vilket ibland kräver att man söker upp spelets information direkt hos spelutvecklaren.

Omsättningskrav och bonusvillkor – så fungerar det i praktiken

Det enskilt viktigaste villkoret att förstå när det gäller gratissnurr är omsättningskravet, på engelska kallat wagering requirement. Detta krav anger hur många gånger en spelare måste omsätta sina vinstpengar från gratissnurren innan de kan tas ut som riktiga pengar. Ett omsättningskrav på 30 gånger innebär att om en spelare vinner 100 kronor från sina gratissnurr, måste denna spela för totalt 3 000 kronor innan pengarna kan tas ut.

Omsättningskrav varierar kraftigt mellan olika casinon och erbjudanden. Historiskt sett har krav på 30 till 50 gånger omsättning varit vanliga inom branschen, men efter Spelinspektionens skärpta regler och den ökade medvetenheten bland svenska spelare har flera aktörer börjat erbjuda lägre krav eller till och med omsättningsfria gratissnurr. Omsättningsfria gratissnurr, ibland kallade wager free free spins, innebär att vinsterna direkt registreras som riktiga pengar utan krav på ytterligare spel. Dessa erbjudanden är generellt mer fördelaktiga ur ett matematiskt perspektiv.

Det finns också tidsgränser att ta hänsyn till. De flesta casinon sätter en tidsgräns på mellan tre och sju dagar för att använda gratissnurren och sedan omsätta eventuella vinster. Om omsättningskravet inte uppfylls inom denna period förfaller bonuspengar och vinster. Dessutom finns det ofta ett maxvinsttak kopplat till gratissnurr, vilket innebär att även om en spelare lyckas vinna ett stort belopp, begränsas den uttagbara summan till ett specificerat maximum, exempelvis 500 kronor eller fem gånger bonusbeloppet.

För den som vill fördjupa sig i hur specifika erbjudanden är uppbyggda och jämföra villkor mellan olika casinon finns det mer information samlad hos specialiserade analyssajter som systematiskt granskar och dokumenterar bonusvillkoren på den svenska marknaden.

En annan aspekt som sällan diskuteras är bidragsprocenten från olika speltyper till omsättningskravet. Många casinon räknar inte alla spel som likvärdiga när det gäller att uppfylla omsättningskravet. Spelautomater bidrar vanligtvis med 100 procent, medan bordsspel som blackjack eller roulette kan bidra med allt från 10 till 0 procent. Detta innebär att om en spelare försöker omsätta bonuspengar via bordsspel, kan processen ta avsevärt längre tid eller vara omöjlig om bidraget är noll.

Spelreglering i Sverige och hur den påverkar gratissnurr-erbjudanden

Den svenska spelmarknaden reglerades om i grunden den 1 januari 2019 när den nya spellagen trädde i kraft. Spelinspektionen, den myndighet som övervakar den svenska spelmarknaden, fick i och med den nya lagen ett tydligare mandat att reglera hur casinon marknadsför sina tjänster och utformar sina bonuserbjudanden. Alla casinon som riktar sig till svenska spelare måste sedan dess inneha en svensk spellicens, och utan licens är det olagligt att erbjuda speltjänster till svenska konsumenter.

Spellagen och Spelinspektionens föreskrifter har haft en direkt påverkan på hur gratissnurr-erbjudanden utformas. Bland annat finns det krav på att bonusvillkor ska presenteras på ett tydligt och transparent sätt, att marknadsföring ska vara måttfull och inte riktas mot utsatta grupper, och att casinon måste erbjuda verktyg för ansvarsfullt spelande som spelgränser och självexkludering. Spelinspektionen har också utfärdat varningar och böter till aktörer som brutit mot dessa regler, vilket har bidragit till att höja standarden på informationen kring bonuserbjudanden.

Under 2020 och 2021 införde den svenska regeringen tillfälliga pandemiåtgärder som ytterligare begränsade bonuserbjudanden. Under denna period tilläts casinon endast erbjuda välkomstbonusar en gång per kund och med begränsade belopp. Dessa restriktioner togs bort när pandemin klingade av, men de visade på statens vilja att aktivt styra hur bonusar används inom spelmarknaden.

Spelföretag som är licensierade utomlands men saknar svensk licens, ofta kallade offshore-casinon, opererar utanför Spelinspektionens tillsyn. Dessa casinon kan erbjuda mer generösa gratissnurr-paket men saknar det konsumentskydd som den svenska regleringen ger. Spel på olicensierade sajter innebär att spelaren inte kan vända sig till svenska myndigheter vid tvister, och att spelskyddsverktyg som Spelpaus inte gäller. CasinosFreeSpins experter betonar vikten av att alltid kontrollera att ett casino har giltig svensk licens via Spelinspektionens officiella licensregister innan man accepterar något erbjudande.

En viktig aspekt av den svenska regleringen är också kravet på att casinon ska identifiera spelberoende beteende och vidta åtgärder. Detta inkluderar att automatiskt begränsa eller stänga konton för spelare som uppvisar riskbeteende. Gratissnurr-erbjudanden kan i teorin fungera som lockbeten som ökar spelfrekvensen, och Spelinspektionen har i sina tillsynsrapporter påpekat att bonusar måste utformas på ett sätt som inte motverkar ansvarsfullt spelande.

Hur spelare bör utvärdera gratissnurr-erbjudanden

Att utvärdera ett gratissnurr-erbjudande kräver mer än att räkna antalet snurr. En strukturerad analys bör ta hänsyn till flera faktorer för att avgöra det verkliga värdet av erbjudandet. Det första steget är att beräkna det nominella värdet av gratissnurren, vilket görs genom att multiplicera antalet snurr med insatsvärdet per snurr. Hundra gratissnurr med ett värde av 1 krona per snurr ger ett nominellt värde av 100 kronor.

Nästa steg är att justera detta värde för spelets RTP. Om gratissnurren gäller på ett spel med 96 procents RTP, är det förväntade utfallet av 100 kronors spel statistiskt sett 96 kronor. Det faktiska förväntade värdet av gratissnurren är alltså inte 100 kronor utan snarare 96 kronor, och detta är innan omsättningskravet räknas in.

Omsättningskravet reducerar det effektiva värdet ytterligare. Om ett omsättningskrav på 30 gånger gäller och casinots husfördel på den aktuella spelautomaten är 4 procent (det vill säga 100 procent minus RTP på 96 procent), innebär ett omsättningskrav på 30 gånger att spelaren i genomsnitt förlorar 30 gånger 4 procent, vilket är 1,2 gånger bonusbeloppet, bara i husfördelar under omsättningsprocessen. Om bonusbeloppet är 96 kronor och omsättningskostnaden statistiskt uppgår till 96 kronor gånger 30 gånger 0,04 = 115 kronor, är det förväntade nettovärdet av erbjudandet negativt.

Denna beräkning förklarar varför omsättningskrav är det viktigaste villkoret att granska. Erbjudanden med låga eller inga omsättningskrav har ett genuint positivt förväntat värde för spelaren, medan erbjudanden med höga omsättningskrav i praktiken fungerar mer som ett sätt att öka spelarens engagemang på plattformen utan att ge ett reellt ekonomiskt fördelaktigt erbjudande.

Experter på CasinosFreeSpins rekommenderar också att spelare granskar vilka spel som är tillåtna för gratissnurren. Ibland är snurren begränsade till spel med lägre RTP eller spel med hög volatilitet, vilket innebär att utfallet är mer oförutsägbart och att sannolikheten för att uppnå det maximala vinsttaket är liten. Volatilitet, eller varians, beskriver hur ofta och hur stora vinster en spelautomat ger. Högvolatila spel kan ge stora enstaka vinster men betalar ut sällan, medan lågvolatila spel ger frekventa men mindre vinster. För att uppfylla ett omsättningskrav kan ett lågvolatilt spel vara mer lämpligt, eftersom det ger en jämnare spelupplevelse och minskar risken att bonuspengar tar slut innan kravet är uppfyllt.

Maxvinsttaket är ytterligare en parameter som begränsar det reella värdet av ett erbjudande. Om ett casino sätter ett maxvinsttak på 500 kronor för gratissnurr-vinster, är det irrelevant om spelaren faktiskt vinner 5 000 kronor under sina snurr – bara 500 kronor kan tas ut. I kombination med omsättningskrav innebär detta att det övre scenariot för en spelare är strängt begränsat, medan casinot fortfarande drar nytta av det ökade spelengagemanget.

Sammanfattningsvis är gratissnurr ett komplext bonusinstrument som kräver noggrann granskning för att spelaren ska kunna fatta välgrundade beslut. De tekniska mekanismerna bakom hur snurren aktiveras och värderas, de regulatoriska ramarna som den svenska spellagen sätter upp, och de matematiska realiteterna bakom omsättningskrav och husfördel är alla faktorer som tillsammans avgör om ett erbjudande faktiskt gynnar spelaren. Transparens och konsumentutbildning är centrala teman i den pågående diskussionen om hur spelmarknaden bör utvecklas, och aktörer som CasinosFreeSpins bidrar till denna diskussion genom att systematiskt analysera och kommunicera hur dessa erbjudanden verkligen fungerar. En spelare som förstår dessa mekanismer är bättre rustad att välja erbjudanden som faktiskt ger värde och att undvika de fallgropar som komplicerade bonusvillkor kan innebära.

CEBA Update – September 2023

At Levr.ai we’ve been keeping a close eye on any changes to the CEBA loan program that is scheduled to come due at the end of this year (2023).

In September, the Canadian government made an announcement regarding a program extension, and many small businesses are a little confused. We don’t blame you! Here’s what you need to know:

- There has been an extension to the repayment deadline from Dec 31, 2023 to Jan 18, 2024 citing that many businesses are extremely busy with year-end activities. These additional 18-days while an extension, for many this falls short of what was expected.

- Another component of the extension announcement is that any CEBA loans not paid in full by Jan 18, 2024 now roll into a 3-year term-loan accruing at 5% per annum (It previously was 2-year term-loan). This update was made in an effort to make monthly installments on outstanding CEBA loans more manageable (smaller).

- The biggest take away is that it’s still better to find a way to refinance your CEBA loan in order to take advantage of the loan forgiveness credit. For many small businesses that continues to be the best overall savings (lowest cost to borrow the full $60K) and the smart option to exercise. Learn more here.

What is CEBA, or a CEBA loan?

CEBA was a government program introduced by the Canadian government in response to the COVID-19 pandemic to provide financial support (through loans) to eligible Canadian small and medium businesses. It offered interest-free loans of up to $60,000 to help small businesses cover their operating costs during the economic downturn caused by the COVID-19 pandemic.

CEBA is administered by Export Development Canada (EDC), which worked closely with Canadian financial institutions to deliver the loans to their existing business banking customers.

CEBA loans were easily available through over 220 Canadian financial institutions in partnership with the Canadian government, CRA and EDC.

The loans are partially forgivable if certain conditions are met, making it a form of financial assistance for qualifying businesses in Canada. Continue reading to learn more about loan-forgiveness options available to small businesses that hold CEBA loans.

What role does Export Development Canada (EDC) play in Canada?

For some small businesses that only did business on Canadian soil before COVID-19, often they were not familiar, or interacted, with Export Development Canada (EDC). Since the inception and availability of CEBA loans—that has changed.

The EDC plays a crucial role in Canada’s international trade and business landscape. As the country’s export credit agency, EDC’s primary mission is to support Canadian businesses in their efforts to succeed globally.

Some of the key roles and functions of Export Development Canada (EDC):

- Export financing

- Export credit insurance

- Market knowledge and research

- Trade risk management

- Foreign investment support

- Access to capital (like CEBA loans)

- Small and medium-sized enterprises (SME) support

Overall, EDC plays a vital role in promoting and strengthening Canada’s position in international trade. By supporting Canadian businesses in their export and foreign investment activities, EDC contributes to economic growth, job creation, and the country’s competitiveness on the global stage.

Are CEBA loans interest-free?

Yes, the CEBA loans are indeed interest-free, offering a ray of light and relief to small business owners during the challenging times brought forth by the COVID-19 pandemic. This compassionate decision by the Canadian government aimed to ease the burden on entrepreneurs and provide them with much-needed financial support without the additional weight of interest charges.

The interest-free nature of the CEBA loans represented more than just a financial advantage. It symbolized empathy, understanding, and a genuine desire to uplift small businesses during their darkest moments. It was a lifeline extended with a warm embrace, a gesture that acknowledged the hardships faced by entrepreneurs and sought to alleviate their worries.

By eliminating the burden of interest, the government sent a powerful message of solidarity. The absence of interest charges reflected a deep understanding of the emotional toll that financial stress can take.

However, any outstanding balance owed by businesses on a CEBA loan beyond the new deadline of December 31, 2023 will be converted to a 2-year term loan at 5 percent interest per annum.

Can I still apply for a CEBA loan?

No, as of 2022 your business cannot get a CEBA loan. The Canadian government closed the application period for the CEBA on June 30, 2021 and the funding period has now ended. As a result, no applications can be submitted, and no new funding will be provided by the CEBA Program.

The Canadian government has said CEBA eligibility criteria validations are complete for all applicants and the results of these validations are final. The opportunity for further resolution has now passed and applications will not be reconsidered by the CEBA Program.

Maximize your CEBA forgiveness credit

Levr.ai can help you find the right loan—it’s easy and fast

What were CEBA loan eligibility requirements?

- Is a Canadian operating business, and has been operating as of March 1, 2020.

- Applicant has a CRA federal tax registration for the business.

- Employment income paid in the 2019 calendar year was between $20,000 and $1,500,000.

- Businesses with $20,000 or less in employment income (2019) must:

- Have a CRA business number and filed a 2018 or 2019 tax return.

- Eligible non-deferrable expenses between $40,000 and $1,500,000. Those eligible non-deferrable expenses could’ve included costs such as rent, property taxes, utilities, and insurance. Expenses were subject to verification and audit by the Government of Canada.

- An active business chequing bank account with the financial institution that extended the CEBA loan, and was the businesses primary financial institution.

- Account was opened on or prior to March 1, 2020 and was not in arrears on existing debt/loans.

What businesses are excluded from the CEBA loan program?

- The business taking a CEBA loan could not be a government organization or body, or an entity owned by a government organization or body.

- Applicants could not have been a union, charitable, religious or fraternal organization or entity owned by such an organization or if it is, it is a registered T2 or T3010 corporation that generates a portion of its revenue from the sales of goods or services.

- The business could not have been owned by any Federal Member of Parliament or Senator.

- The business cannot promote violence, incite hatred or discriminate on the basis of sex, gender identity or expression, sexual orientation, colour, race, ethnic or national origin, religion, age, or mental or physical disability, contrary to applicable laws.

How much did the Canadian government loan to small businesses via CEBA loans?

CEBA loans provided much-needed financial relief during the tumultuous times of the COVID-19 pandemic.

In total, the Canadian government offered up to $60,000 through the CEBA program. Any small businesses that opted for only $40,000 in funding were able to apply for an additional $20,000 of financing through the CEBA program. Nearly 600,000 businesses took advantage of this extension under the CEBA program.

This injection of funds aimed to help small businesses stay afloat, preserve jobs, and navigate the stormy economic waters caused by the pandemic.

The Canadian government has provided great transparency on the CEBA program statistics stating it had approved CEBA loans for 898,271 Canadian businesses. CEBA loans totaled $49.2 Billion of approved funds, this money injected into the Canadian economy for small businesses to survive and thrive pre and post COVID-19 pandemic.

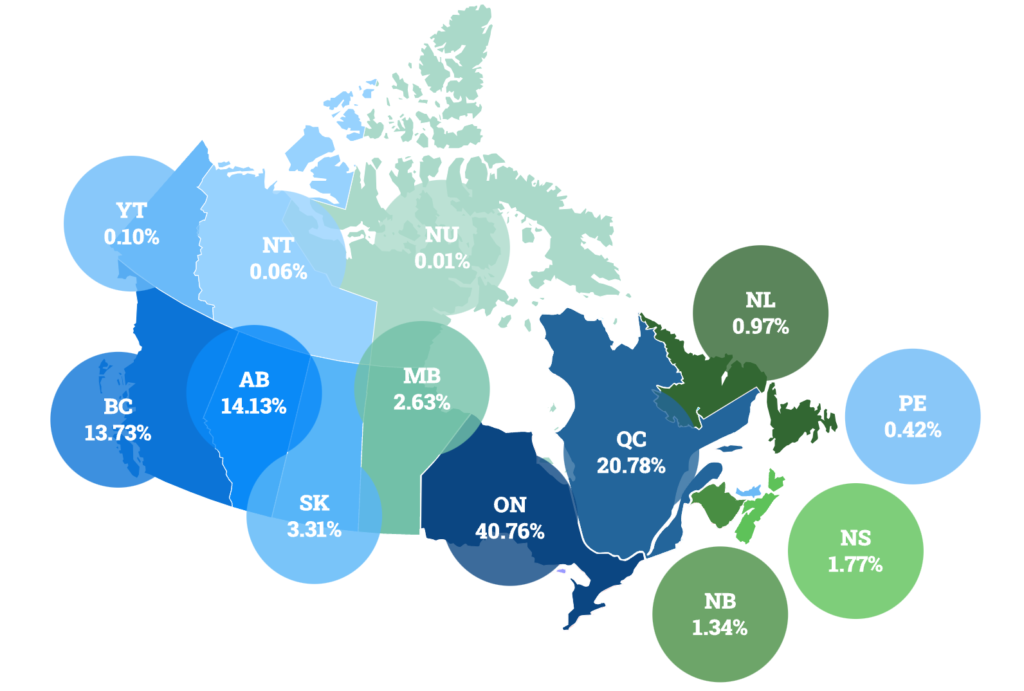

From a regional perspective businesses located in the province of Ontario received the most funding of nearly $20 Billion across 360,339 loans. Second was the province of Quebec, with $10 Billion funded across 182,923 loans. In third, the province of Alberta with roughly $7 Billion funded across about 125 thousand small businesses. For a complete breakdown of CEBA loans by Canadian provinces visit the Canadian government website.

– Canadian Government CEBA Program Statitics – Jun 2023")

CEBA summary data as of January 26, 2022 (modified April 24, 2023)

1 “CEBA loans” refer to $40,000 and $60,000 loans; “CEBA expansions” refer to $20,000 expansions provided to businesses with an existing CEBA loan

2 Funding approved by the Government of Canada may take up to 2 business days to be disbursed to CEBA applicants

3 Total excludes CEBA loans where applicants and/or Financial institutions have not provided provincial or territorial information

This financial support meant more than just numbers on a balance sheet. It allowed small business owners to continue paying their dedicated employees, covering rent and utilities, and meeting other essential expenses. It helped maintain the vibrancy of local Canadian communities.

The Canadian government’s decision to lend a helping hand to small businesses through the CEBA loans showcased the profound understanding of the human stories behind these ventures. It recognized the tireless efforts, sacrifices, and dreams of countless entrepreneurs who pour their hearts and souls into their businesses.

Is the government extending the payback date for CEBA loans beyond December 31, 2023?

At this time, there isn’t any information from the Canadian government and its organizations CRA or EDE about extending the payback period beyond the December 31, 2023 deadline.

There are a number of groups lobbying for an extension, like the NDP of Canada and Canadian Federation of Independent Business (CFIB) to name a few.

The Canadian government extended the payback date for CEBA loans, in 2022 to the end of 2023 demonstrating their understanding and empathy towards the challenges faced by small businesses during the COVID-19 pandemic. While another year has quickly passed and there are a number of small businesses across Canada hoping for another (unlikely) extension.

Why are CEBA loans due at the end of 2023?

The decision to set the due date for CEBA loans at the end of 2023 was undoubtedly a result of careful consideration and understanding of the unique circumstances faced by small businesses during the COVID-19 pandemic. It was a response born out of empathy and a desire to provide breathing room for struggling entrepreneurs.

However with rising interest rates, the government has alluded it’s time for it to reappropriate this investment to help fund other business assistance programs.

The last extension on CEBA loan deadline for payback was recognition that recovery has taken more time for small businesses to recover from COVID-19 pandemic impacts and regain stability.

The end of 2023 as the due date symbolized a new beginning—a fresh start for small businesses. It represented an opportunity to turn the page on the difficulties of the pandemic era that is ending and embark on a journey towards renewed prosperity.

The decision to set the due date for CEBA loans at the end of 2023 was a tangible demonstration of the government’s belief in the resilience and tenacity of small business owners to continue to recover post COVID-19 pandemic.

Levr.ai can help you find the right loan—it’s easy and fast

Maximize your CEBA forgiveness credit

What is the CEBA loan forgiveness and do you qualify?

The Canadian government is extending up to 33 percent (or up to $20,000) loan forgiveness on outstanding CEBA loans of $60,000. If your business only took $40,000 of CBEA loans, you’ll be able to take advantage of up to 25 percent (or up to $10,000) loan forgiveness.

In order to qualify for the loan forgiveness of up to $20,000 on CEBA loans your business must be in good standing with the Canada Revenue Agency (CRA). And you must repay a portion of the CEBA loan on or before the December 31, 2023 deadline.

CEBA loan forgiveness is determined by the amount borrowed.

CEBA loans of $40,000 or less you must repay $30,000 by Dec 31, 2023 to receive $10,000 of CEBA loan forgiveness. CEBA loans of $60,000 you must repay $40,000 to receive $20,000 of CEBA loan forgiveness. Note that any value of loan forgiveness is still subject to regular business taxes.

For the businesses that opted for the CEBA expansion, if you received a $40,000 loan and subsequently received the $20,000 expansion, the terms of your forgiveness have changed and are described by the Canadian government as follows:

Repaying the outstanding balance of the loan (other than the amount available to be forgiven) on or before December 31, 2023 will result in a single tranche of loan forgiveness up to $20,000 based on a blended rate:

- 25 percent on the first $40,000; plus

- 50 percent on amounts above $40,000 and up to $60,000.

For clarity, the portion of forgiveness based on a rate of 25 percent and the portion of forgiveness based on a rate of 50 percent are combined into a single tranche of forgiveness, which is only available if all other amounts outstanding are repaid by December 31, 2023. For example, if $60,000 is borrowed, no forgiveness is available unless $40,000 is repaid.

Note: some financial institutions may record your $40,000 loan and $20,000 expansion as two separate loans. For the purposes of loan forgiveness, borrowings and repayments on both loans will be aggregated.

What if I already repaid my first CEBA loan?

If you fully repaid your original $40,000 loan, claimed forgiveness, and thereafter received the $20,000 expansion. Repaying the outstanding balance of the $20,000 expansion (other than the amount available to be forgiven) on or before December 31, 2023 will result in loan forgiveness of 50 percent (up to $10,000).

How do I find the balance owed on my CEBA loan?

If you contact your financial institution that provided the funds you will be able to know the balance owing on your CEBA loan.

The Canadian government worked with over 200 financial institutions to distribute CEBA loans. It was encouraged to work with an institution that you also did everyday business banking with for the business, it’s likely your usual business banking institution.

Options if you cannot payback your CEBA loan.

Option 1: The Canadian government will be supporting the conversion of CEBA loans to a 2-year term loan at 5 percent interest per annum. This new business term loan will be facilitated through the financial institution that originally provided your CEBA loan in 2020.

While this seems like a smart and fair option – 5 percent interest is affordable considering the recent increased cost of borrowing in 2023. For those who use the full 2-years to pay back the loan, the cost to continue borrowing CEBA funds will be approximately $6,150 in interest on $60,000 CEBA principal.

Option 2 – THE BETTER OPTION – work with Levr.ai and explore how you can borrow the minimum amount required to pay back your CEBA loan and be eligible for loan forgiveness value. Think of this forgiveness as a discount or free money—because it is!

Let’s run the numbers, you’d be surprised that for MANY BUSINESS option 2 is the best option.

Example: you borrowed the full $60,000 and you’re in good standing with the CRA. This means if you pay back $40,000 on or before the Dec 31, 2023 deadline you’ll receive $20,000 of forgiveness.

Before the deadline you work with a certified lender to borrow $40,000 and get the max of $20,000 in loan forgiveness. This new $40,000 loan at 18 percent interest (per annum) over 2-years (say with a monthly payment of $1,997) will cost you $7,927 in interest. If you take $20,000 less the cost of borrowing for additional 2-years you still are up $12,073. Paying a total of $47,927 for $60,000 in funding.

The smarter option is clearly Option 2 vs. Option 1 of simply keeping the CEBA loan outstanding, do not receive any loan forgiveness, and pay an additional $6,150 costing you $66,150 for $60,000 in CEBA funding.

Book a free call with a Levr.ai lender expert and get as much as you can for loan forgiveness on your CEBA loan before Dec 31, 2023. Alternatively, you can create a FREE Levr.ai account, provide some quick information about your business and see all your loan options for over 25 certified lenders.

Maximize your CEBA forgiveness credit

Levr.ai can help you find the right loan—it’s easy and fast

If you have more questions about your CEBA loan, available is the CEBA Call Centre at 1-888-324-4201 operated by the Canadian government. The CEBA Call Centre is available Monday to Friday from 9AM to 6PM Eastern Standard Time (EST), excluding statutory holidays.

Levr.ai can help take the pain out of finding the RIGHT financing optional for your business to get what it needs fast, and keeps your business growing.

Now that you have a better understanding of the ins and outs of CEBA loans, it’s important to review all your options. If you have experience applying for a business loan (really any kind of business loan) you will already know the work involved can be time-consuming.

Levr.ai is designed to make this process easier, faster, and more straightforward. A safe and secure platform allows you to collaborate with the key members of your team i.e. accounting, financial planner, and business operators to organize all the required financial statements and necessary business forecasts, plans, and documents. Having everything in one place makes it easier to apply with multiple lenders to secure the rates and loan repayment terms that are best for your business.

In addition to making the process of getting a loan better, Levr.ai’s free loans marketplace allows you to review options and compare offers from multiple lenders based on what is right for you and what allows you to achieve your growth goals.

Levr.ai also can negotiate exclusive loan rates with its expert team of certified financial advisors and loan industry partnerships.

To learn more about Levr.ai and business term loan options in the free loans marketplace, create a free account today.

Important information: Levr.ai provides financial education services in the form of blogs, posts, templates, and support documents and are intended to inform and educate readers on various financial topics, including but not limited to budgeting, investing, and small business finance. Levr.ai’s website and/or blogs etc. (mentioned above) are not to be confused with a certified accountant or financial advisor, and the information provided should not be construed as professional advice.

Clients are solely responsible for their financial decisions and actions, and Levr.ai is not liable for any damages or losses that may result from such decisions or actions. The information provided is general in nature and may not be suitable for all individuals or situations.

Clients are encouraged to seek the advice of a certified accountant or financial advisor for specific financial advice tailored to their individual circumstances. Levr.ai does not endorse any specific financial products or services and is not responsible for any third-party information or links provided.

By using Levr.ai’s financial education tools, clients acknowledge and accept these terms and any conditions of liability. For more additional information about our Terms of Service or Privacy Policy click the respective embedded links or navigate to our website footer.